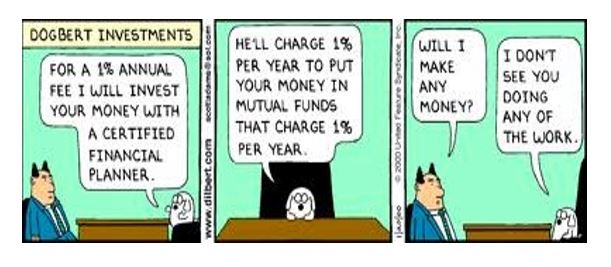

When it comes to investing money, many people seek advice from a financial adviser. This is not unusual and financial adviser can add value to enhance your long term wealth. The cost of investing your money is best described as scaled, but asymmetrical. The more you make, the more you lose in fees. And the incentives are such that it is better for the manager to invest all of your money rather than just some of it with a store of cash.

Now if they add value that is fine however most managers underperform the wider market and so you are paying fees to lose money (politely referred to as underperformance). That does not make sense.

Advisers can charge a flat annual fee or in some cases a percentage of your assets that they manage – for example 1%. In most cases these advisers will recommend that you place your money in a fund that also charges fees. So in some cases, you can be hit with two sets of fees – one from the adviser and one from the recommended fund.

There are various fees and charges when you invest in a managed fund and funds don’t all charge fees in the same way. Active fund managers (who buy and sell a lot of stocks during the year) incur higher taxes due to the large number of transactions. This in turn reduces the investment returns of the fund. Over a 25 year period, an investor would hand over a shocking 30.5% of his/her income just to receive the average long term return.

{kind=link}

{kind=link}