Arguably, diversification is the number one principle that you will receive from an overwhelming majority of financial advisers or planners. Diversification has been promoted as a standard refrain for a long time as a way to reduce risk in a portfolio. The risk of putting all you funds in just one or two stocks is risker than putting it in one or two hundred. Hence diversification is the mantra, and so most investment portfolios look alike, made up of a residential property, some shares and a superannuation account (which is usually more weighted in stocks).

Another reason to diversify was according to the Efficient Market Hypothesis, you can’t beat the overall market and so the best approach was to simply buy the index and receive the market return. Trying to select companies that will outperform all the other was near nigh impossible, so don’t bother.

Buffett said that diversification is for folks who don’t know what they’re doing. He’s not rude, but simply stating that unless you want to spend a lot of time looking a company balance sheets and the “fundamentals” (I’ve had a life of it so wouldn’t recommend it) you should heed his advice – buy and index fund, sit back and collect the pot when you retire.

But the problem for many people is that they won’t have enough for retirement, and so you could be excused for asking if just buying an index fund (diversification) is the best approach or is there a potentially better way?

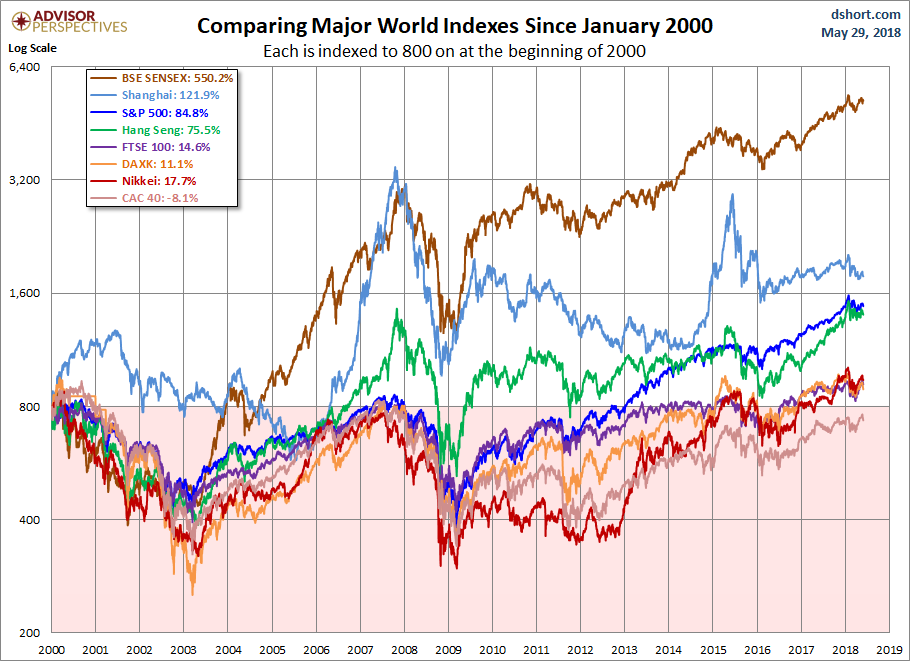

Since the 80’s there has been an increasing linkages between each country’s economy as they expand trade in goods and services As each country connects, their stock markets also starts to increase their correlation. If you look at the graph below, you see that most of the major markets move in some kind of sync. What varies is the level of returns.

{kind=link}

{kind=link}